Getting an adverse action notice can feel confusing, especially if you expected an approval or you are not sure what went wrong. This notice is meant to give you clarity and next steps. Below is a straightforward explanation of what it is, what it typically includes, and how to respond.

What an adverse action notice means

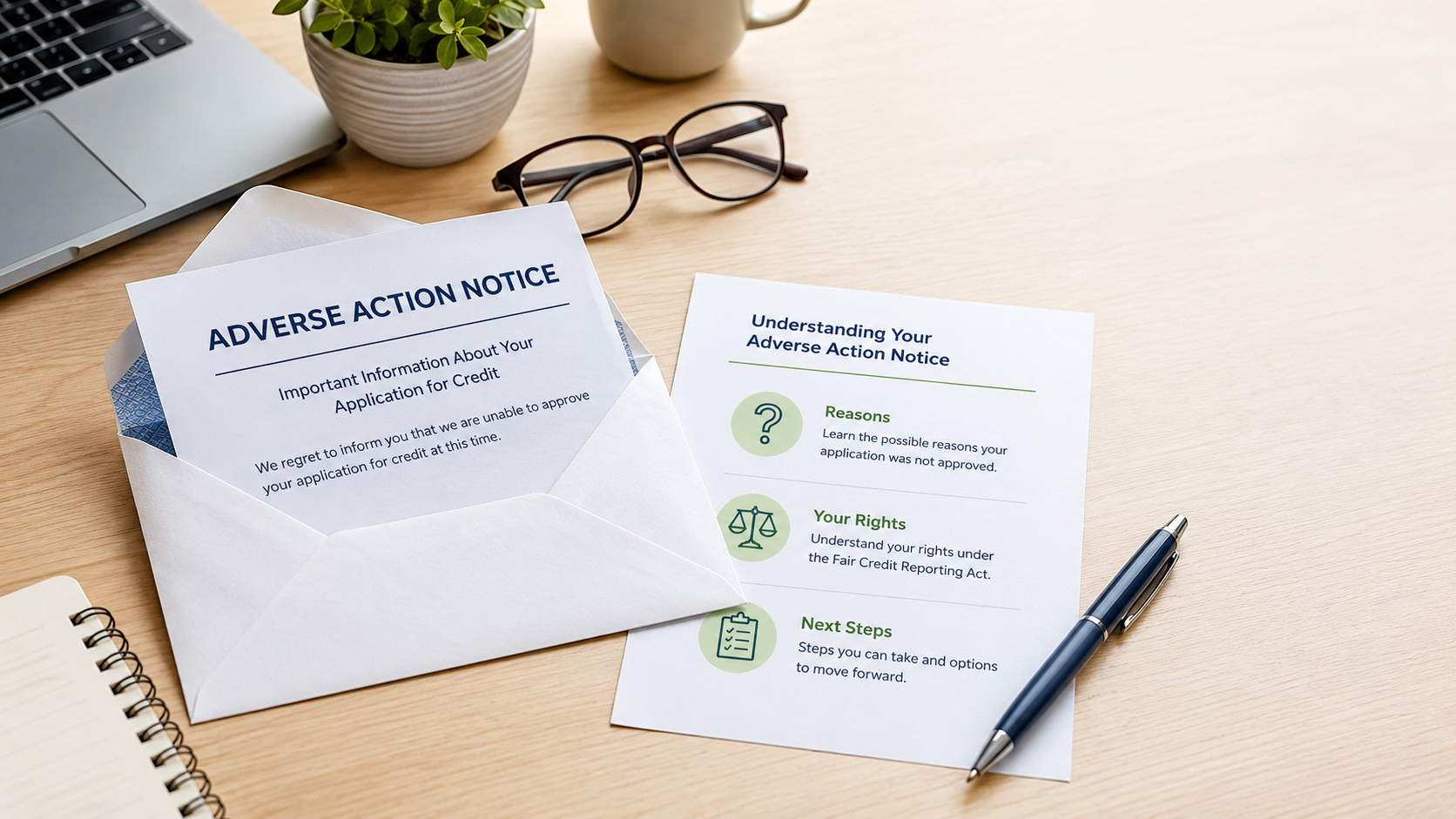

An adverse action notice is a formal notice that tells you a credit decision did not go your way. Most commonly, it means your application was denied. In some situations, it can also mean you were not approved for the specific terms you requested, or the lender is offering different terms instead.

You may receive this notice by mail or electronically.

When you might receive one

Borrowers most often receive adverse action notices after applying for credit, such as:

- An installment loan or signature loan

- A credit card or line of credit

- A request to change credit terms, depending on the action taken

You may also see the phrase “adverse action” in other situations like employment, housing, or insurance decisions, but this article focuses on loans and credit.

Why lenders send adverse action notices

Adverse action notices exist to help consumers understand a denial or other unfavorable decision, and to explain certain rights you may have when consumer reporting information was used.

Two common federal frameworks that apply are:

- ECOA and Regulation B: generally require lenders to provide specific reasons for denial or tell you how to request those reasons. Reasons must be specific, not vague.

Source: Consumer Financial Protection Bureau Regulation B, section 1002.9. - FCRA: if a consumer report influenced the decision, the notice typically includes the consumer reporting agency’s contact info, your right to a free copy of your report within a set timeframe, and your right to dispute inaccuracies.

Source: Federal Trade Commission guidance on adverse action notices.

What is typically included in an adverse action notice

Many notices include:

- Your name and address

- The primary reason or reasons for the decision

- If a consumer report was used, the name and contact details of the consumer reporting agency

- A statement that the consumer reporting agency did not make the decision and cannot explain it

- Your right to request a free copy of your report and your right to dispute inaccuracies, if applicable

Notices often list a few principal reasons rather than every factor considered.

Common reasons borrowers receive an adverse action notice

Here are frequent reasons and what they usually mean in plain language:

Incomplete or unverifiable information

Missing documents, inconsistent details, or information that cannot be verified.

Income does not meet requirements

Income may be below a minimum threshold, or the requested payment may not be affordable given other obligations.

Debt to income is too high

Existing monthly debt payments may already take up too much of your monthly income.

Limited credit history

You may have a thin credit file or not enough history to evaluate risk.

Negative credit history signals

Late payments, defaults, or high balances can affect a decision. If you believe information is incorrect, you can review and dispute it.

Too many recent applications

Multiple recent credit inquiries can signal elevated risk.

Your rights after receiving an adverse action notice

1) Request your consumer report

If a consumer report played a role, you typically have the right to request a free copy within the period stated in the notice.

Source: FTC adverse action guidance.

2) Dispute errors

If you find inaccurate or incomplete information, you can dispute it with the consumer reporting agency.

Source: FTC adverse action guidance.

3) Receive specific reasons, not generic wording

Regulation B requires reasons to be specific enough to be meaningful.

Source: CFPB Regulation B, section 1002.9.

The CFPB has also emphasized that lenders still must provide meaningful reasons even when decisions involve complex algorithms.

What to do next, step by step

- Read the reasons listed on the notice

Treat them like a checklist. They point to what needs to change before reapplying. - If a consumer reporting agency is listed, request your report

Review personal details, account accuracy, balances, and any items that look unfamiliar. - Dispute incorrect items quickly

Wrong addresses, accounts that are not yours, duplicate late payments, or incorrect balances can be worth disputing. - Fix what you can control right away

Provide missing documents, correct application details, and consider paying down revolving balances if possible. - Reapply with a right sized request

If the reasons relate to affordability, requesting a smaller amount can improve payment fit.

Pre adverse action vs adverse action

You may hear “pre adverse action” more often in hiring contexts, where an organization shares information first to give you time to respond before a final decision. In lending, borrowers typically receive the final adverse action notice that explains the decision.

- Get your free credit reports: https://www.annualcreditreport.com

- FTC guide to adverse action notices: https://www.ftc.gov/business-guidance/resources/using-consumer-reports-credit-decisions-what-know-about-adverse-action-risk-based-pricing-notices

- CFPB Regulation B adverse action rules: https://www.consumerfinance.gov/rules-policy/regulations/1002/9/

- CFPB guidance on adverse action and algorithms: https://www.consumerfinance.gov/compliance/circulars/circular-2022-03-adverse-action-notification-requirements-in-connection-with-credit-decisions-based-on-complex-algorithms/

Quick FAQ

Does an adverse action notice mean I can never be approved?

No. It means the application did not meet requirements at that time. Many issues are fixable.

Why does the notice list only a few reasons?

Notices commonly list the principal reasons rather than every factor reviewed.

If the decision used automation, can the reasons be vague?

The expectation remains that reasons should be specific and meaningful.

What to do if you have questions

If you received an adverse action notice and want help understanding the next steps, Money 4 You can walk you through what the notice means and what information may be needed if you choose to apply again.

Here is the best way to get support:

- Have your adverse action notice available so you can reference the listed reason codes.

- Confirm your personal information matches your current ID and address.

- Gather basic documents such as proof of income and proof of address, in case the notice relates to missing or unverifiable information.

- Ask what can be updated or verified on a new application, such as income details, employment information, or documentation.

What we can do:

- Explain the general meaning of the reasons listed on your notice

- Tell you what documents are typically used to verify information

- Help you understand what updates may strengthen a future application

What we cannot do:

- Change information from a consumer reporting agency

- Override underwriting requirements

- Guarantee approval on a future application

If your notice references a consumer reporting agency, you can also request a copy of your report and dispute any inaccuracies directly with that agency. That is often the most effective step when the notice indicates a report related reason.

Quick Loan Application

Get started on your Short Term Installment Loan Application from Money 4 You Loans